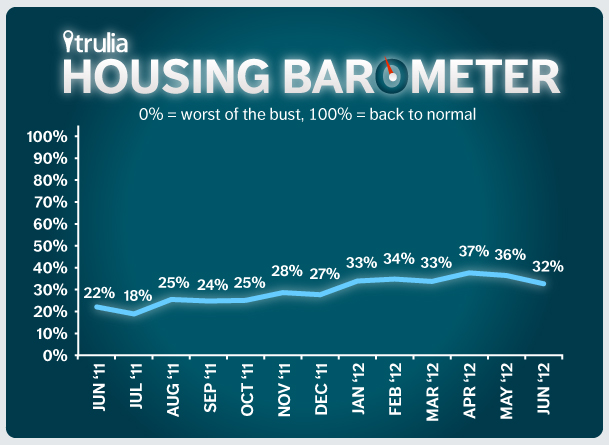

Each month, Trulia’s Housing Barometer charts how quickly the housing market is moving back to “normal.” We summarize three key housing market indicators: construction starts (Census), existing-home sales (NAR) and the delinquency-plus-foreclosure rate (LPS First Look). For each indicator, we compare this month’s data to (1) how bad the numbers got at their worst and (2) their pre-bubble “normal” levels.

In June 2012, construction starts improved, but existing home sales fell and the delinquency + foreclosure rate rose:

—Construction starts jumped. Starts rose in June to a 760,000 annualized rate, up 7% month-over-month and 24% year-over-year. Construction activity was especially strong in Texas and the Carolinas. Now, construction starts are 28% of the way back to normal.

—Existing home sales fell sharply, from 4.62 million in May to 4.37 million in June. Now, home sales are just 35% back to normal to from their worst point during the bust, down from 49% in May: they’re now much closer to their low of November 2008 than to their pre-bubble normal level. That’s a big slide. Tighter inventory, especially of distressed homes, held back sales.

—The delinquency + foreclosure rate went up. In June, 11.23% of mortgages were delinquent or in foreclosure, up from 11.08% in May. (LPS revised its historical data, which changed our barometer measure slightly.) The delinquency + foreclosure rate is 34% back to normal, down a bit from 36% in May.

Averaging these three back-to-normal percentages together, the market is now 32% of the way back to normal – the lowest level in 2012 but still well above June 2011, when the market was 22% back to normal.

Cause for concern? Depends who you are. We’re farther from normal mostly because of the big drop in home sales, which was due to tightening inventory: fewer homes for sale means fewer sales. However, tighter inventory is part of the process of recovery. In fact, inventory nationally is now near its long-term normal level – even though it is tight relative to several years of unusually high inventory. Tighter inventory is good news for sellers, who face less competition. But it’s bad news for buyers, who face fewer choices and higher prices. And, of course, tighter inventory and lower sales are bad news for many in the real estate industry who depend on sales. The housing barometer shows that the road to recovery is bumpy and uneven.