The housing market rides the seasons. Year in and year out, market activity has predictable ups and downs. Sometimes those seasonal patterns are hard to see when longer-term trends (like plummeting housing prices) or one-off events (like the homebuyer tax credit) drive movements in prices, sales and other housing indicators. But seasonal patterns are there, even when they’re beneath the surface.

To understand the effects of long-term trends or one-time events on the market, housing wonks like to “seasonally adjust” data. That means we strip out the regular seasonal patterns in order to highlight trends or events. This is useful for deciding whether the market is really in recovery or assessing the impact of a housing policy.

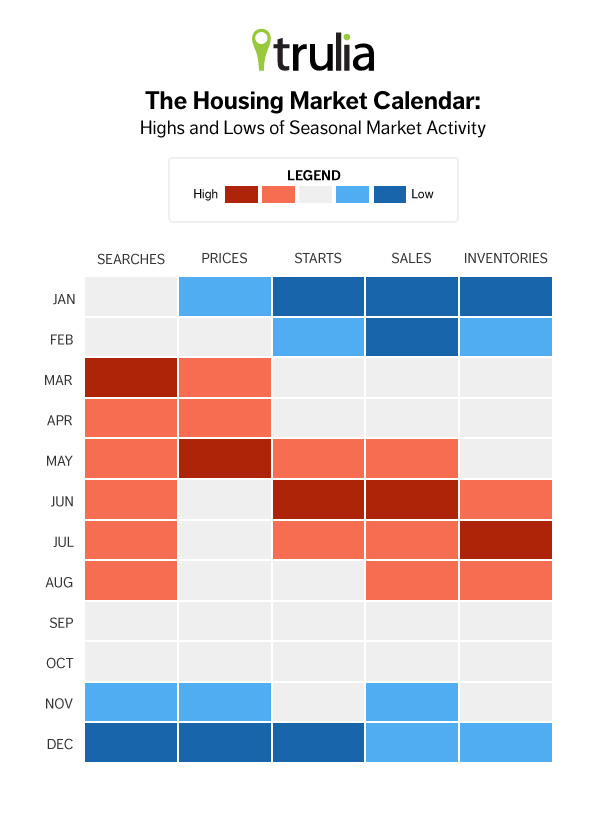

But these seasonal patterns help show us what’s really going on in the housing market, which is important because they give us hints about when we should search, list, buy, sell or build. In this post, I look at five measures of housing activity: search activity (Trulia), asking prices (Trulia), new construction starts (Census), existing home sales (NAR) and housing inventory (deptofnumbers.com).

Starts and Sales Swing with the Seasons

New construction starts and existing home sales fluctuate more throughout the year than other housing activities. The chart below shows that sales are typically 29% above their annual average in June and 31% below their annual average in January. Construction starts also swing 25% above and below their annual average over the year. No wonder builders and agents say theirs are seasonal businesses. Other activities float rather than swing with the seasons. Search activity rises 12% above its annual average in March. But inventories stay within 10% of their annual average every month, and asking prices stay within 5% of their annual average every month (see note below on asking prices).

The Spring Thaw Comes First to Buyers, then to Sellers

As the market comes out of winter hibernation, buyers wake up first. The table below shows when each measure hits its highs and lows. In the winter, all activity rests: searches, prices, starts, sales and inventories all slide to their yearly low in December or January. Life resumes in March, as search activity pops up and stays above normal through August. Prices rise too and reach their annual high in May. Summer has endings and beginnings: sales peak in June, as do new construction starts. But inventory keeps climbing as some sellers miss the sales peak, topping out in July and August.

What do these patterns tell us? Homebuyers are a little ahead of sellers. Asking prices peak at the start of the season, so demand appears to rise ahead of supply. As supply catches up, prices ease back down and sales peak. After that, inventories build up a bit further through the summer.

High-Season Comes Stronger and Later in the North

High-Season Comes Stronger and Later in the North

Harsh climates fuel seasonality. It’s harder to build homes in the snow, and a lot less fun to go to open houses (or host them). Construction starts in the Midwest are 2.5 times higher in June than in January, but in the South, construction starts are only 50% higher at the summer peak than at the winter low. Sales seasonality too is stronger in the Midwest and Northeast than in the South and West.

The best time to buy or sell? Depends on where you are. If you want to buy when inventory swells (or want to avoid those months for selling), inventory peaks in the summer across most of the country, but not in the Sunbelt. In Miami, Tampa and Orlando, inventory peaks in March; Las Vegas inventory peaks in October, and Phoenix inventory peaks in December – just in time to buy a home for Christmas.

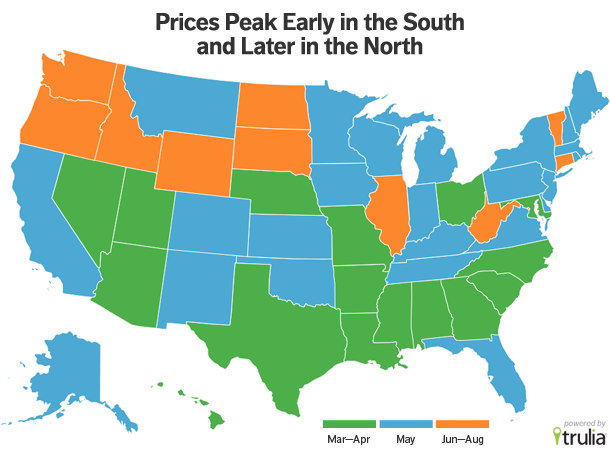

Looking to buy low or sell high? Nationally, asking prices peak in May and bottom in December, so sellers can get top dollar in the spring, while buyers can find bargains later in the year. In other words, buyers should be more patient than they are, while sellers should move faster to get their home on the market. But prices tend to peak earlier in the South, as the map below shows, and later in the North, so the best deals come later in the year the farther North you are. And the harshest climates create the biggest swings: prices for similar homes vary more with the seasons in Minnesota, Illinois and Maine than in any other state.

Technical Details:

— All data presented are the seasonal factors from the Census X-12 seasonal adjustment model, applied to at least five years of unadjusted raw data from each source. As each data source allows, I estimated separate seasonal factors for each metro, state, or region as well as for the US overall.

— Asking-price data from Trulia.com are adjusted for housing characteristics and neighborhood attributes. Therefore, the seasonal pattern in asking prices is not affected by seasonal changes in the types of homes that get listed.