Potential buyers are discovering that it’s becoming harder to find starter and trade-up homes, but expensive luxury homes are flooding the market. Nationally, our housing market mismatch score for all homes has grown to 14.7 from 9.2 over the past year, reflecting a marketplace that’s becoming more unbalanced.

Market mismatch is our measure of search interest compared with available listings. On a scale of 0 to 100, with 0 being perfectly matched and 100 being completely mismatched, it’s a measure of the difference between the price points where searches occur and the price points of listed properties. For example if all searches in a market occurred in the starter category, but all listings were in the premium category, the market would be completely mismatched and receive a mismatch score of 100. Alternatively, if 20%, 50%, and 30% of listings were starter, trade-up, and premium listings respectively and 20%, 50%, and 30% of all search activity was for starter, trade-up, and premium homes, then the market would be perfectly matched a have a mismatch score of 0.

For this edition of Mismatched Markets, we took a closer look at what’s driving the expanding (or contracting) gap between what people are searching for and what is available nationally and in the 100 largest U.S. metros. We compared home searches and for-sale inventory on Trulia between April to June (Q2 2017) from a year ago (Q2 2016).

At the same time that premium listings are saturating the market nationally, searches for starter and trade-up are making up a larger share of all search activity. This is trouble for most first-time homebuyers, especially when put in the context of historically low inventory across all price ranges.

For some metro areas there are noticeable deviations from this narrative. Here are some key takeaways from our analysis:

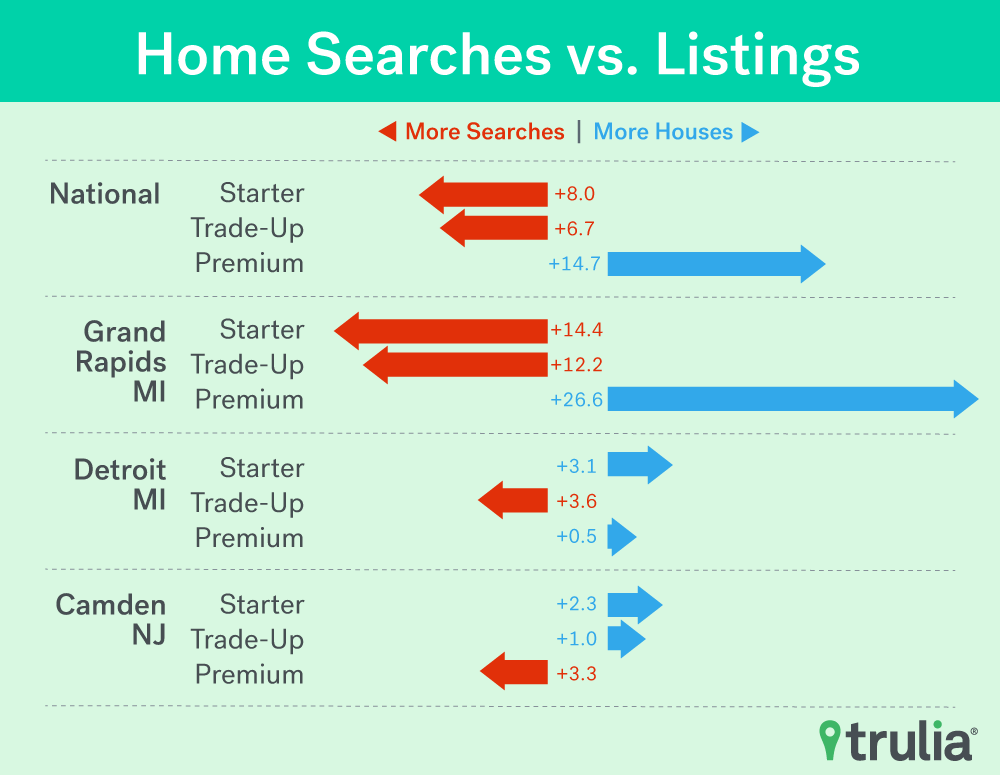

- Nationally, the mismatch gap has grown as the share of starter and trade-up listings has decreased to 45.8% of all listings from 46.5% a year ago. Meanwhile, searches for starter and trade-up homes has risen to 60.5% from 55.6%.

- This means starter and trade-up home buyers are increasingly getting pinched with an 8.0 and 6.7 percentage point shortfall of listings relative to search interest, respectively.

- …and premium home buyers have both more options and less competition. There is now a 14.7 percentage point surplus of listings relative to search interest in the premium price category.

- Houston – until Hurricane Harvey – was the most unbalanced market in the country, mostly due to its shortage of starter and trade-up homes. While it’s still too early to know the full impact on the local housing market, we do expect to see changes in market mismatch in the coming months; the nature of which will depend on how home developers, buyers, and sellers respond to a post-Harvey economy.

- Luxury problems: top end listings flooded the market in Richmond, Va., at the same time that a smaller portion of search activity was directed at these properties. The percentage point gap between the searches and listings nearly doubled to 17.3 from 8.9.

- Motown is moving: Detroit – one market where searches historically were aimed at more expensive homes – the market mismatch fell the most, going from 11.1 to 3.6 as the surplus of cheap homes disappeared from the listings.

<!–[if IE 9]>

<!–[if IE 9]><![endif]–>

While all inventory fell during the last year, starter and trade-up home inventory fell more. At the same time, millennials and other first time home buyers are coming back into the market that they were largely excluded from by tight lending standards and higher unemployment. Additionally, those whose credit reports were rocked by a foreclosure during the recession may be seeing those scores recover (7 years is the standard time it takes for foreclosures to no longer affect credit scores) and are also back in the market. Hence the double whammy for starter and trade-up home shoppers; lots of competition being met with dwindling options.

Houston and Beyond

Recovery efforts are underway in Houston. There are certain to be dramatic changes in the housing market. A shifting balance between what people want and what is available is unavoidable. From hurricanes Katrina and Sandy, we know that impacts on prices tend to be much more strongly influenced by larger macroeconomic trends than by immediate effects of the storm. There were large increases in building permits in New Orleans more than a year after Hurricane Katrina and in New York almost 3 years after Hurricane Sandy. Given the rapid economic and population growth Houston has seen over the past decade, it seems unlikely that the city would experience a similar population loss anywhere near that of New Orleans in the aftermath of Hurricane Katrina. Given the cities’ building history, it would also make sense that building activity will be comparatively responsive to the lost supply of available housing.

Taking a more local look elsewhere, during the past year, market mismatch grew in 88 of largest 100 metro areas. Some of the largest market mismatch increases over the past year occurred in places like Richmond, Columbus, Ohio, and Grand Rapids, Mich. Grand Rapids is now the second most mismatched market in the country, up from 14th a year ago. In all three of these cities, from Q2 2016 to Q2 2017, there was a dramatic fall in the share of listings considered starter homes, met with a large increase in the proportion of searches for these same starter homes. Trade-up homes in these places were a bit more stable from both a listing and search perspective, but this means that all the listing losses in the starter categories were made up for by proportional gains in the premium category. Similarly, the rise in proportion of searches for starter and trade-up homes has come at the expense of premium homes. So listing availability and search traffic are moving in opposite directions.

<!–[if IE 9]>

<!–[if IE 9]><![endif]–>

Where Inventory Is Closer to Demand

Of the 12 metro areas that saw a decrease in their market mismatch, the largest improvements occurred in places like Detroit, Philadelphia and Phoenix. Detroit has had a pretty unique listing-to-search traffic fingerprint in that it is one of the few places where there is consistently a surplus of starter homes relative to search interest. The city was experiencing chronic net out-migration and home value depreciation well before the Great Recession. This had left the area with an unusually large stock of dilapidated homes; the product of years of neglect brought on by economic decline. Since 2014 though, the city has demolished more than 12,000 blighted homes and employment growth has outpaced the national rate for much of the past 2 years. The effects of employment growth and proactive housing policy efforts seem to be having the effect of reducing the surplus of junk listings in the starter category.

Phoenix, on the other hand, while having a more common search/listing fingerprint with a shortage of starter and trade-up homes relative to search interest, has seen its mismatch score fall over the past year from 16.2 to 13.3. Driving this change was an uptick in the proportion of starter and trade-up homes, going from 12.9% and 28.2% of listings last year to 14.8% and 30.9% this year, respectively. While the proportion of traffic directed at premium homes fell to 40.9% in Q2 2017 from 42.7% in Q2 2016 and shifted mainly into the starter category, this was not enough to offset the decline in listings.

With mortgage rates remaining favorable and unemployment low, the homebuying waters probably seem welcoming enough to bring out more home buyers, many of them younger and first timers. But with inventories at historic lows and the make-up of that inventory continuing to slide away from the make-up of home buyer interests, we expect many starter and trade-up home buyers are going to find a competitive market with few options, with the possible exception of those in a handful of unique markets.

Methodology

Note: The calculation for the market mismatch was adjusted from the first two installments of this report. This means the numbers between this installment and the previous one are not directly comparable. However, all the data presented in this report was pulled using the updated method.

Additionally, while the same price cut-offs are used to define starter, trade-up, and premium homes nationally and in the 100 largest U.S. metros as in the quarterly Trulia Price and Inventory Watch, the weights assigned to listings differ, resulting in some differences in the inventory make-up. This different weighting was necessary to ensure that we are only counting site traffic to properties when they are actively on the market.

The Market Mismatch Score was based on all the for-sale listings on Trulia, which were pulled on a quarterly basis beginning in Q4 2014. The distribution of prices for each metro and nationally was calculated by taking each active listing and adding up the number of days it was on the market during the quarter. All unique price points were consolidated and counted by summing these day & price combinations. In other words, if 10 properties were on the market for a combined 600 days at a price of $200,000, then the $200,000 price point would receive a weight of 600.

Site traffic from Trulia was matched to each unique property (and therefore price) on the market during the same time periods and added up for each quarter and price.

Listings and searches were assigned starter, trade-up, and premium price categories based on the price. “Market Mismatch” scores were then calculated by taking the difference between the percentage of listings in each of the three price tiers and the percentage of site traffic that went to each price tier. The average deviation from 0, regardless of the sign of the difference (+/-), for each category was averaged to come up with an overall mismatch score.