U.S. home inventory tumbled to a new low in the first quarter of 2017, falling for eight consecutive quarters. Homebuyers have now been stifled by low inventory for the last two years despite prices rising to pre-recession highs in many markets.

In this edition of Trulia’s Inventory and Price Watch, we examine how home value recovery may be limiting supply in markets that have recovered most. We find that homebuyers in markets with the biggest gains are facing the tightest supply.

The Trulia Inventory and Price Watch is an analysis of the supply and affordability of starter homes, trade-up homes, and premium homes currently on the market. Segmentation is important because home seekers need information not just about total inventory, but also about inventory in the price range they are interested in buying. For example, changes in total inventory or median affordability don’t provide first-time buyers useful information about what’s happening with the types of homes they’re likely to buy, which are predominantly starter homes.

Looking at the housing stock nationally and in the 100 largest U.S. metros from Q1 2012 to Q1 2017, we found:

- Nationally, the number of starter and trade-up homes continues drop, falling 8.7% and 7.9% respectively, during the past year, while inventory of premium homes has fallen by just 1.7%;

- The persistent and disproportional drop in starter and trade-up home inventory is pushing affordability further out of reach of homebuyers. Starter and trade-up homebuyers need to spend 2.9% and 1.6% more of their income than this time last year, whereas premium homebuyers only need to shell out 0.9% more of their income;

- A strong recovery may be partly to blame for the large drop in inventory some markets have experienced over the past five years. On average, the more valuable a market’s housing is compared to pre-recession levels, the larger drop in inventory it is has seen.

2017 Ushers in a Dramatic Shortage of Homes

Nationally, housing inventory dropped to its lowest level on record in 2017 Q1. The number of homes on the market dropped for the eighth consecutive quarter, falling 5.1% over the past year. In addition:

- The number of starter homes on the market dropped by 8.7%, while the share of starter homes dropped from 26.1% to 25.9%. Starter homebuyers today will need to shell out 2.9% more of their income towards a home purchase than last year;

- The number of trade-up homes on the market decreased by 7.9%, while the share of trade-up homes dropped from 23.9% to 23%. Trade-up homebuyers today will need to pay 1.6% more of their income for a home than last year;

- The number of premium homes on the market decreased by 1.7%, while the share of premium homes increased from 50% to 51%. Premium homebuyers today will need to spend 0.6% more of their income for a home than last year.

| 2017 Q1 National Inventory and Price Watch | ||||||||

| Housing Segment | 2017 Q1 Inventory | Change, 2016 Q1 – 2017 Q1 | ||||||

| Median

List Price |

Share | Inventory | % of Income Needed to

Buy Median Price Home in Segment |

% Change in Median

List Price |

Percentage

Point Change in Share |

% Change in Inventory | Additional Share of Income

Needed to Buy a Home (Percentage -Point Change) |

|

| Starter | $165,015 | 25.9% | 253,735 | 38.3% | 8.3% | -0.2 pts | -8.7% | +2.9 pts |

| Trade-Up | $289,455 | 23.0% | 229,585 | 25.6% | 6.8% | -0.9 pts | -7.9% | +1.6 pts |

| Premium | $614,143 | 51.0% | 497,231 | 14.0% | 7.2% | +1.0 pts | -1.7% | +0.9 pts |

| Among the 100 largest U.S. metro areas. Share is the percent of for-sale homes that fall into each segment, which is defined separately for each metro. Median price for each segment is the stock-weighted average of the median price of each segment in each metro. Some point change estimates may be slightly different than stated values because our differing procedure occurs before rounding. The full data set can be downloaded here. | ||||||||

How and Where a Strong Housing Market May Be Hurting Inventory

In the first edition of our report, we provided a few reasons why inventory is low: (1) investors bought up much of the foreclosure home inventory during the financial crisis and turned them into rental units, (2) price spread – that is, when prices of homes in different segments of the housing market diverge from each other – makes it difficult for existing homeowners to tradeup to the next the segment, and (3) slow home value recovery was making it difficult for some homeowners to break even on their homes. While there is evidence that investors indeed converted owner-occupied homes into rentals as well as evidence from our first report that increasing price spread is correlated with decreases in inventory, little work has examined how home value recovery affects inventory. This is perhaps due to the tricky conceptual relationship between home values and inventory: too little recovery might make it difficult for homeowners to sell their home but cheap to buy one, while too much recovery might make it easy for them to sell but difficult to buy.

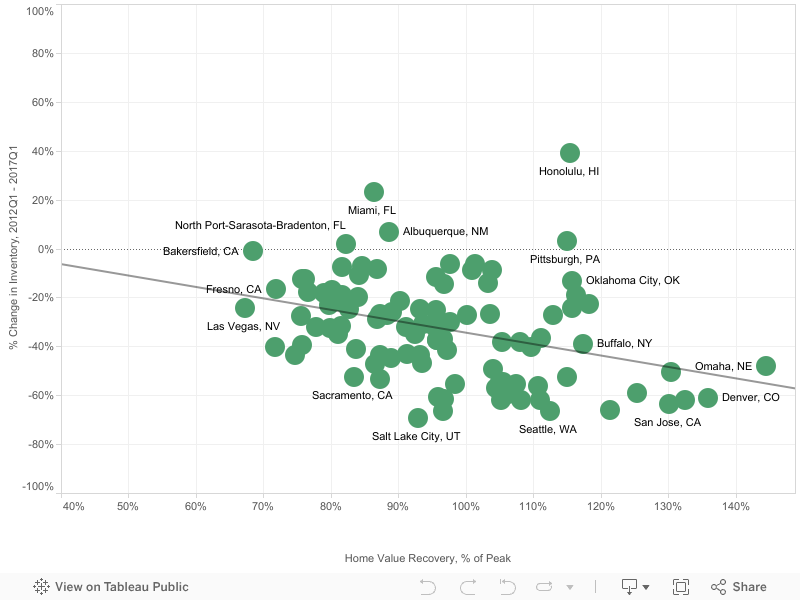

In fact, we find a negative correlation between how much a housing market has recovered and how much inventory has changed over the past five years. Using the current value of the housing market relative to the peak value as our measure of recovery, we find markets with greater home value recovery have experienced larger decreases in inventory over the past five years. The linear correlation was moderate (-0.36) and statistically significant. We also found that markets with the strongest recovery, on average, have experienced the largest decreases in inventory.

For example, the five-year average change in inventory of housing markets currently valued below their pre-recession peak (< 95% of peak value) isn’t that different from ones that have recovered to 95% – 105% of their peak. (-27.6% vs. -30.1%). However, the average change in inventory in well-recovered markets (> 105%) is 0more drastic at -45.4%.

The disparity also persists when looking at changes in inventory within each segment, although the difference is largest for starter homes. On average, markets with less than 95% recovery or 95% to 105% recovery had a 34.2% and 31.7% decrease in starter inventory, while markets with more than 105% home value recovery had a whopping 58.2% drop. These findings suggest that a moderate home value recovery doesn’t affect inventory much, but a strong recovery does and impacts inventory of starter homes the most.

Methodology

Each quarter, Trulia’s Inventory Monitor provides three metrics: (1) the number and share of inventory that are starter homes, trade-up homes, and premium homes, (2) the change in share and number of these homes, and (3) the affordability of those homes for each type of buyer. For the first edition of this report, we back-calculate inventory for each quarter back to the first quarter of 2012 through the first quarter of 2016.

We define the price cutoffs of each segment based on home value estimates of the entire housing stock, not listing price. For example, we estimate the value of each single-family home and condo and divide these estimates into three groups: the lower third we classify and starter homes, the middle third as trade-up homes, and the upper third as premium homes. We then classify a listing as a starter home on the market if its listing price falls below the price cutoff between starter and trade-up homes. This is a subtle but important difference between our inventory report and others. This is because the mix of homes on the market can change over time, and can cause large swings in the price points used to define each segment. For example, if premium homes comprise a relatively large share of homes for sale, it can make the lower third of listings look they’ve become more expensive when in fact prices in the lower third of the housing stock are unchanged.

Our national metrics are a weighted sum of listings and weighted average of affordability of the 100 largest metropolitan areas and our inventory measure is an average of snapshots taken on the first of each month of the quarter. Last, we measure affordability as the share of income needed to purchase the median priced home in each segment relative metro household income terciles. To lessen the downward skew of income of households in the lowest tercile, we estimate starter homebuyer’s income using only household incomes of homeowners within this segment.