America is experiencing a housing shortage. Not only are there fewer homes available to buyers of all income levels, those just starting out or making their first foray into home ownership are worse off than they’ve been in years. There are fewer homes available, an even if they can find a home, it’s likely to be more expensive.

Compared to other inventory reports, the Trulia Inventory and Price Watch is a new quarterly report that offers buyers and sellers deeper insight into the supply and affordability of homes within different segments: starter homes, trade-up homes, and premium homes.

Home seekers need information not just about total inventory, but also about inventory in the segment they are interested in buying. For example, changes in total inventory or median affordability don’t provide first-time buyers useful information about what’s happening with starter homes. In addition, there is also a strong relationship between inventory and affordability in the three segments, so it’s important to track segment changes because that change is likely to induce change inventory and affordability in other segments.

Looking at all the housing stock nationally and in the 100 largest U.S. metros from January 1, 2012 to March 1, 2016, we found:

- Nationally, inventory has dropped most for starter and trade-up homes, but less so for premium homes;

- Regionally, starter home inventory is down most in the West and South. Starter home affordability is down most in California;

- Rising prices is causing homebuyer gridlock. The growing price spread between premium homes and trade-up homes in some markets is highly correlated with fewer trade-up homes coming onto market.

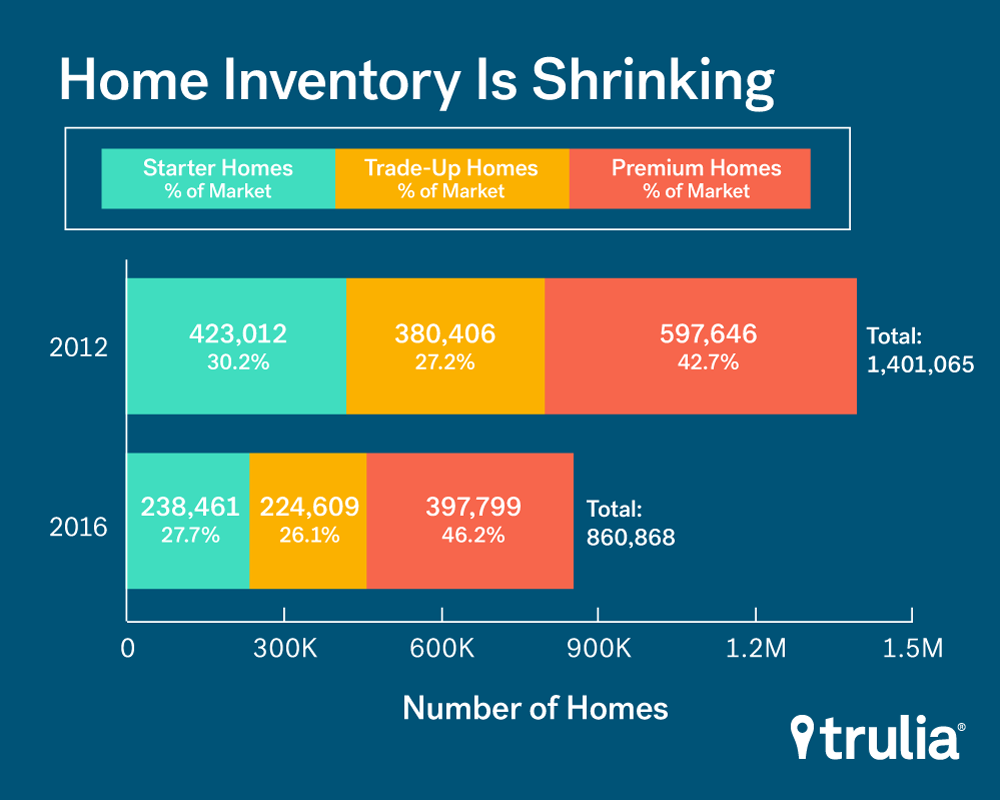

Nationally, Starter and Trade-Up Home Inventory Down More Than 40% Since 2012

Heading into the spring house-hunting season, inventory remains tight and affordability is worsening, especially for starter-home buyers. Over the past four years:

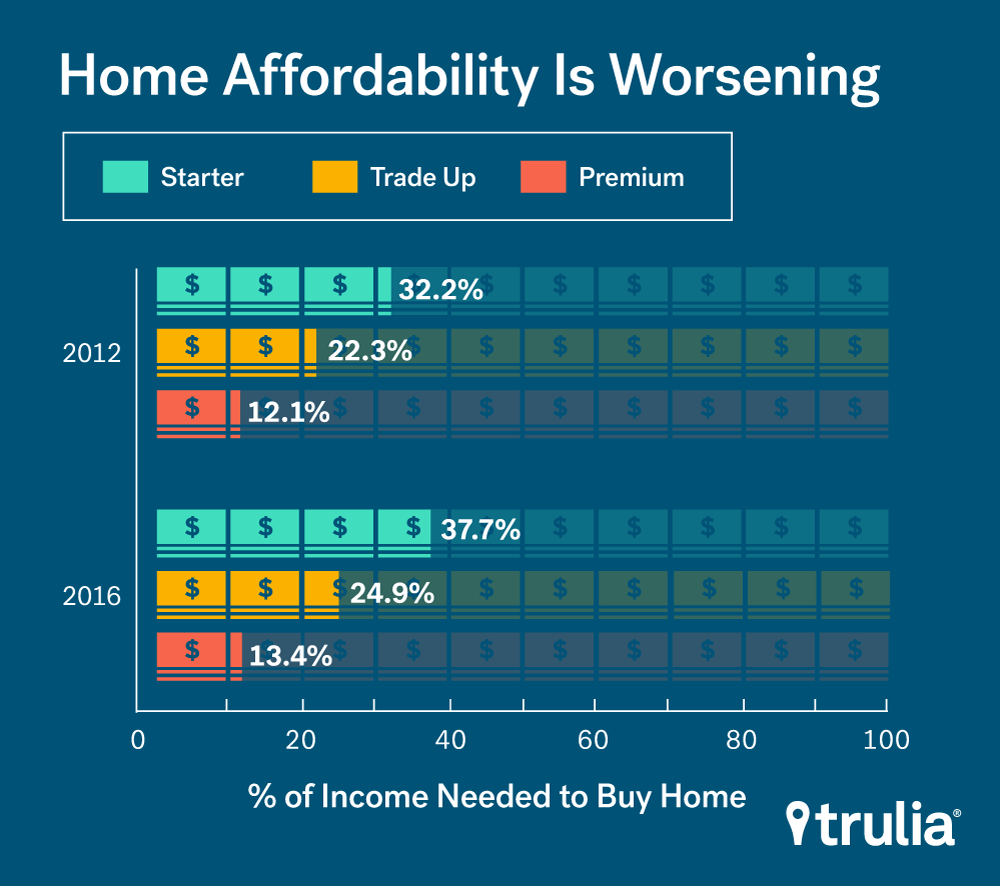

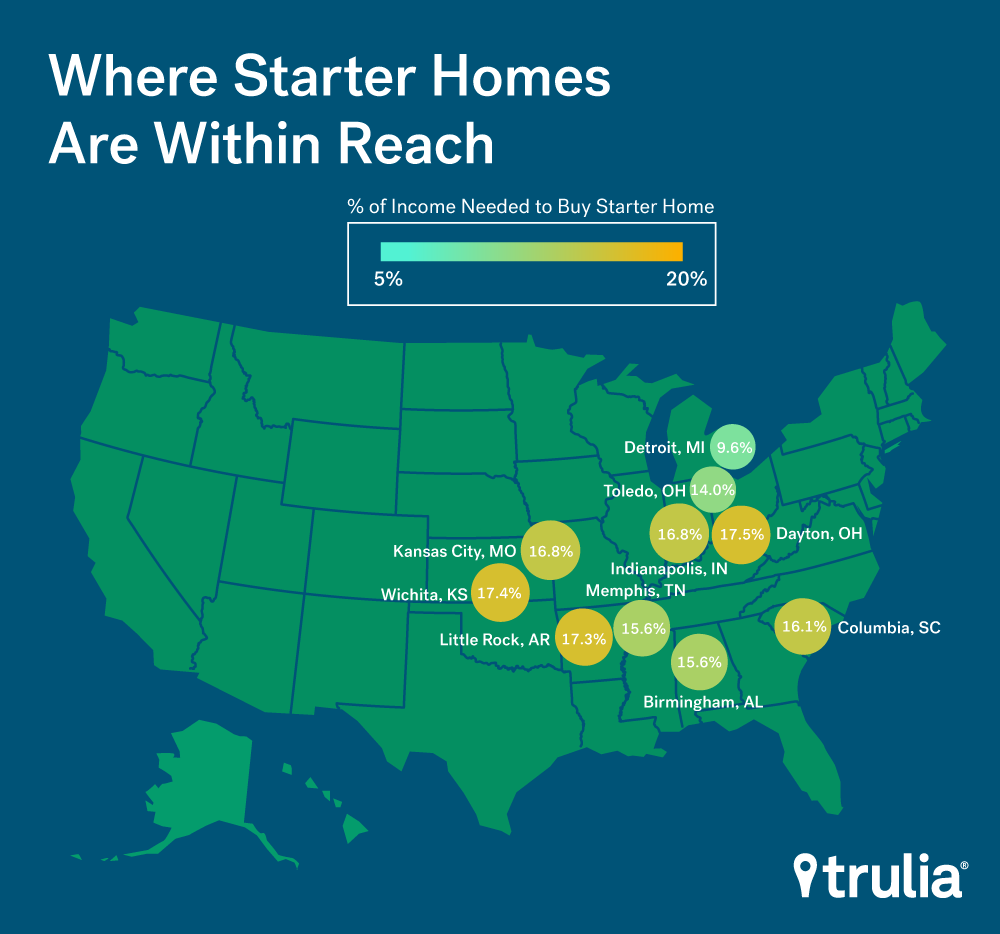

- The number of starter homes on the market dropped by 43.6%, while the share of starter homes dropped from 30.2% to 27.7%. Starter homebuyers today will need to shell out 5.6% more of their income — based on the median income of start-up buyers — towards a home purchase than in 2012;

- The number of trade-up homes on the market decreased by 41%, while the share of trade-up homes dropped from 27.2% to 26.1%. Trade-up homebuyers today will need to pay 2.6% more of their income for a home than in 2012;

- The number of premium homes on the market decreased by 33.4%, while the share of premium homes increased from 42.7% to 46.2%. Premium homebuyers today will need to spend 1.4% more of their income for a home than in 2012.

| National Inventory and Price Watch | |||||||||

| 2016 Q1 Inventory | Change, 2012 Q1-2016 Q1 | ||||||||

| Housing Segment | Median List Price | Share | Inventory | % of Income* | % Change in Median List Price | % Point Change in Share | % Change in Inventory | Added Share of Income* (% Point Change) | |

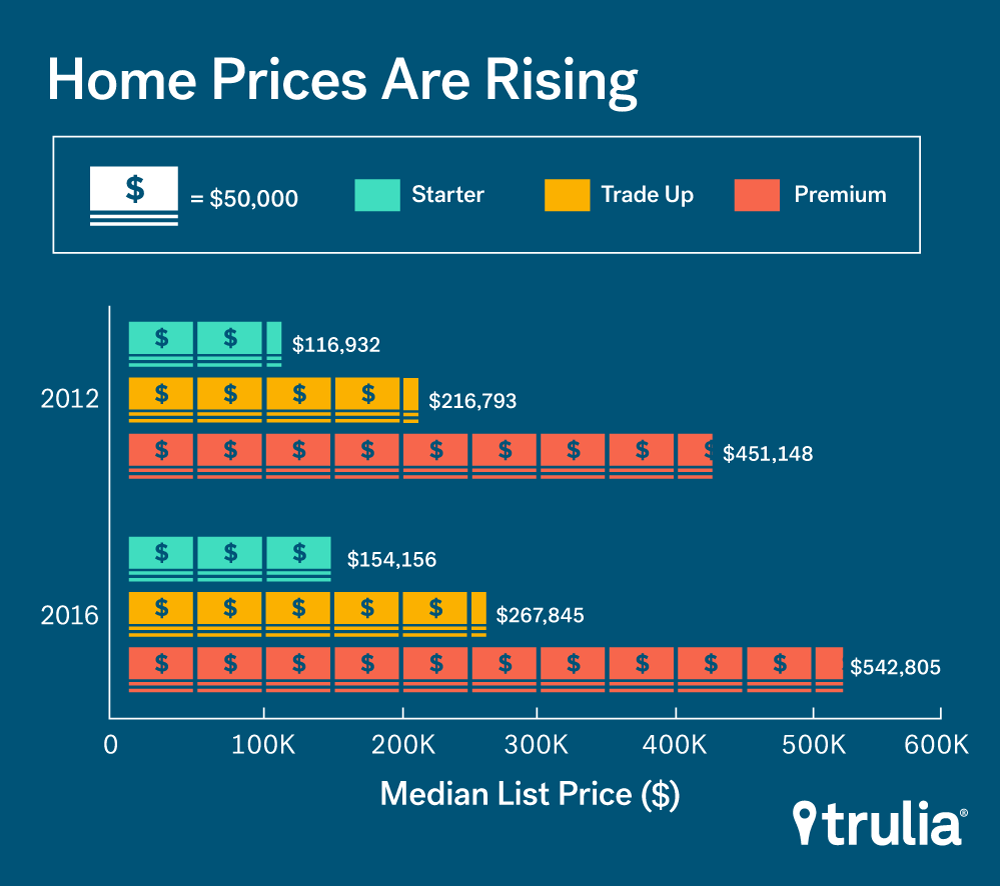

| Starter | $154,156 | 27.7% | 238,461 | 37.7% | 31.8% | -2.5% pts | -43.6% | +5.6% pts | |

| Trade-Up | $267,845 | 26.1% | 224,609 | 24.9% | 23.5% | -1.1% pts | -41.0% | +2.6% pts | |

| Premium | $542,805 | 46.2% | 397,799 | 13.4% | 20.3% | +3.5% pts | -33.4% | +1.4% pts | |

| Among the 100 largest U.S. metro areas, full data available here. Share is the percent of for-sale homes that fall into each segment, which is defined separately for each metro. Median price for each segment is the stock-weighted average of the median price of each segment in each metro. Some point change estimates may be slightly different than stated values because our differing procedure occurs before rounding. | |||||||||

| *Needed to buy median price home in segment | |||||||||

Low inventory is taking a toll on the affordability of all home segments, but especially starter homes. At the bottom of the housing market in 2012, starter homes were nearly affordable, primarily because starter prices were discounted: homebuyers needed only to shell out 32.2% of their income to buy the median priced starter home. Now, starter homebuyers would need to dedicate 37.7% of their income – a 5.6 percentage point increase. This is significantly more than the 2.6 and 1.4 percentage point increase in income that trade-up and premium homebuyers need to spend, respectively.

Why is inventory so low, especially for starter and trade-up homes? Three reasons: First, investors bought many of the foreclosed homes during the recession and turned into rentals. Second, a larger share of lower-priced are homes are still underwater compared to premium homes, which means that these homeowners are unlikely to sell and take a loss. Third, and most importantly, rising prices are creating homebuyer gridlock. In other words, the spread of homes prices, specifically the growing difference between premium homes prices and trade-up home prices, is likely causing a decrease in trade-up home inventory.

Why does the premium price spread matter? The more premium home prices rise, the more difficult it is for trade-up homeowners to find a premium home that fits their budget. And if trade-up homeowners can’t find a home that fits their budget, they are less likely to sell their existing home. In fact, there is a strong correlation between growth in the premium home price gap and a drop in the inventory of trade-up homes. In other words, housing segments are intertwined. The more premium prices rise, the less likely existing trade-up homeowners will put their home on the market.

For Starter Homebuyers, Wrangling a Home out West is Tough

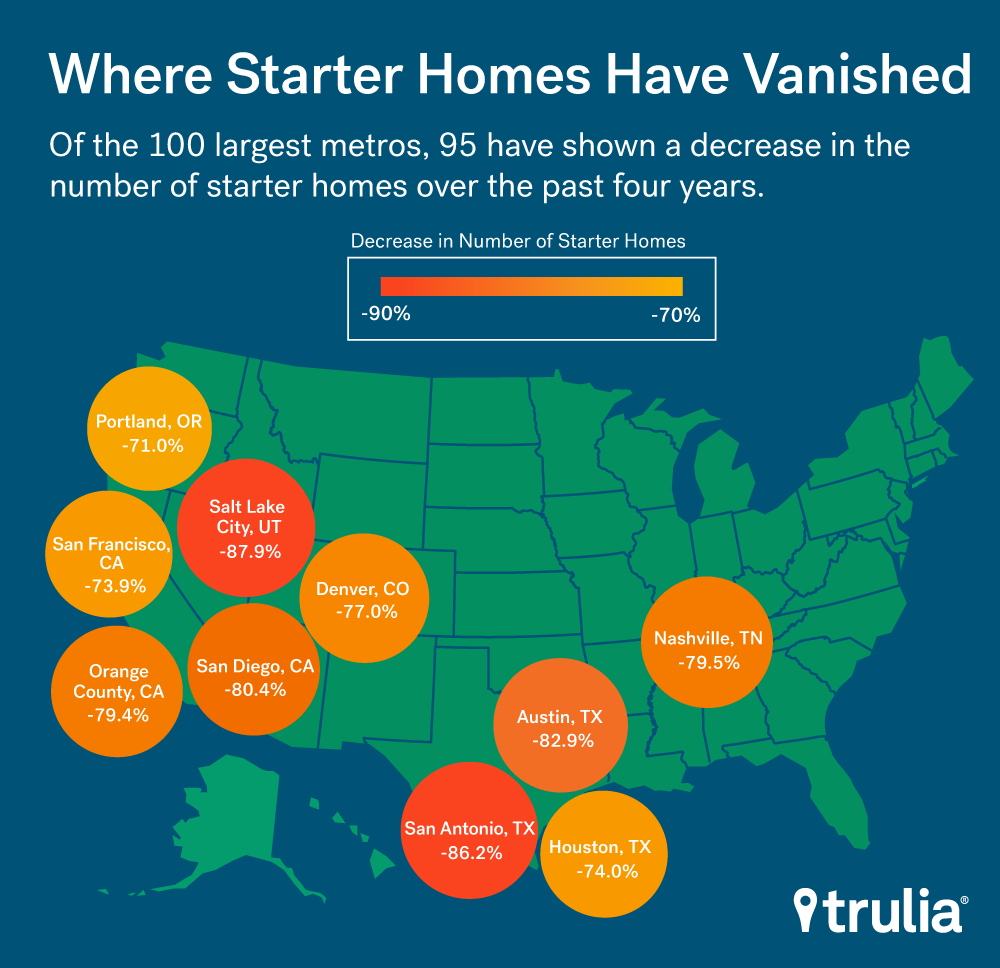

Across the 100 largest metros, 95 have shown a decrease in the number of starter homes over the past four years. Of the 10 metros that have seen the largest drop, all are in the West and South. The number of starter homes in Salt Lake City has dropped the most, from 1,243 to just 151 – an 88% drop in four years.

| Markets with Largest Decrease in Starter Homes | |||

| U.S. Metro | Starter Home Inventory, 2012 Q1 | Starter Home Inventory, 2016 Q1 | % Change in Starter Home Inventory |

| Salt Lake City, UT | 1,243 | 151 | -87.9% |

| San Antonio, TX | 3,097 | 426 | -86.2% |

| Austin, TX | 1,927 | 329 | -82.9% |

| San Diego, CA | 4,415 | 864 | -80.4% |

| Nashville, TN | 3,383 | 694 | -79.5% |

| Orange County, CA | 4,088 | 841 | -79.4% |

| Denver, CO | 2,321 | 534 | -77.0% |

| Houston, TX | 7,448 | 1,934 | -74.0% |

| San Francisco, CA | 606 | 158 | -73.9% |

| Portland, OR-WA | 2,526 | 732 | -71.0% |

| NOTE: Among the 100 largest U.S. metro areas, full data available here. | |||

Starter Home Affordability Worsens in California

The list of metros with the largest decrease in starter home affordability – which is affected by both the number of listings and home-buying demand – looks rather different. Nine of the 10 metros experiencing the largest drop in affordability are located in the Golden State. For instance, starter-home buyers in Oakland, Calif., would have to spend nearly 70% of their income to afford a 30-year fixed-rate mortgage on a starter home, which is 29% more of their income than in 2012.

The cause of this sharp drop in California’s starter-home inventory: demand for starter homes remains high because of strong job growth. Faced with growing demand and tight supply, prices of all homes in California have risen sharply over the past few years. And as prices rise, homebuyers tend to follow the principles of supply and demand.

This means buyers must settle for smaller, less expensive homes than they might otherwise buy elsewhere. Some of this substitution effect could play out in the form of homebuyers increasingly looking down the housing ladder – those who might normally buy trade-up homes might actually be looking at buying smaller, less expensive homes that fall into the starter home category, inflating prices past the affordability points for true starter-home buyers.

| Markets with Largest Decrease in Starter Home Affordability | ||||

| U.S. Metro | Median Starter Home List Price, 2016 Q1 | % of Median Starter-Home Buyer Income Needed to Buy Median-Priced Starter Home, 2016 Q1 | Additional Share of Income Needed to Buy Starter Home in 2016 Q1 vs. 2012 Q1 | |

| Oakland, CA | $374,000 | 69.2% | +29.0% pt | |

| Los Angeles, CA | $329,000 | 88.1% | +28.2% pt | |

| San Jose, CA | $585,713 | 86.7% | +26.6% pt | |

| San Francisco, CA | $714,000 | 110.5% | +24.7% pt | |

| Sacramento, CA | $217,900 | 54.3% | +23.3% pt | |

| Orange County, CA | $416,000 | 78.2% | +22.6% pt | |

| Ventura County, CA | $375,575 | 65.6% | +19.8% pt | |

| Miami, FL | $130,000 | 46.3% | +19.2% pt | |

| San Diego, CA | $327,450 | 68.6% | +18.1% pt | |

| Riverside, CA | $177,450 | 48.2% | +16.8% pt | |

| NOTE: Among the 100 largest U.S. metro areas, full data available here. The additional share of income needed to purchase the median priced home is a percentage point chain from 2012 Q1 to 2016 Q1. | ||||

Prospective first-time and trade-up homebuyers should consider that if the inventory of homes for sale continues to drop, finding a home will remain difficult. They likely will be faced with more competition for the few homes that are on the market, which can lead to bidding wars and homes selling higher than asking price. Sellers are in an increasingly better position to sell their home than in years past, but may have trouble finding another home to buy. Ultimately, premium home buyers will have a much better shot at finding a home, since over 46% of the listings in the last three months were in this segment.

Methodology

Each quarter, Trulia’s Inventory Monitor provides three metrics: (1) the number and share of inventory that are starter homes, trade-up homes, and premium homes, (2) the change in share and number of these homes, and (3) the affordability of those homes for each type of buyer. For the first edition of this report, we back-calculate inventory for each quarter back to the first quarter of 2012 through the first quarter of 2016.

We define the price cutoffs of each segment based on home value estimates of the entire housing stock, not listing price. For example, we estimate the value of each single-family home and condo and divide these estimates into three groups: the lower third we classify and starter homes, the middle third as trade-up homes, and the upper third as premium homes. We then classify a listing as a starter home on the market if its listing price falls below the price cutoff between starter and trade-up homes. This is a subtle but important difference between our inventory report and others. This is because the mix of homes on the market can change over time, and can cause large swings in the price points used to define each segment. For example, if premium homes comprise a relatively large share of homes for sale, it can make the lower third of listings look they’ve become more expensive when in fact prices in the lower third of the housing stock are unchanged.

Our national metrics are a weighted sum of listings and weighted average of affordability of the 100 largest metropolitan areas and our inventory measure is an average of snapshots taken on the first of each month of the quarter. Last, we measure affordability as the share of income needed to purchase the median priced home in each segment relative metro household income terciles. To lessen the downward skew of income of households in the lowest tercile, we estimate starter homebuyer’s income using only household incomes of homeowners within this segment.