When it comes to buying a home, Americans have been feeling the crunch in recent years. Demand is high, inventory is low, and prices continue to rise. These pressures have created a perfect storm for prospective buyers – they now need to pay more for a home, and will likely have a hard time finding that home.

In today’s squeezed environment, it can feel like the going is tougher than ever before – certainly, tougher than our parents had it. But were the good old days really that good? Trulia took a look at home affordability across the decades to try to answer this question.

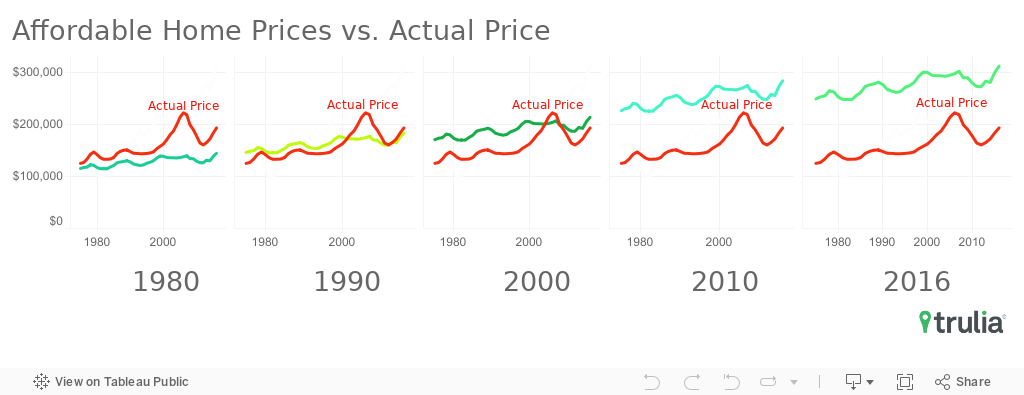

We constructed an affordability score, comparing the highest price the median household could afford with median actual home prices in each year. A household’s highest affordable price is its maximum buying power, with a 20% mortgage down payment. An affordability score of 100 means that the affordable and actual prices are exactly the same; a score of 100 or higher means housing is affordable, and under 100 means it is not affordable. In other words, an affordable market is one in which the median household income’s buying power meets or exceeds the median home price – even if prices are high, if household incomes are high enough to cover that price, then the market is considered affordable.

Using this score, we were able to determine whether housing was affordable (i.e., whether the affordability score was above 100), and how affordable housing was, compared to previous years (i.e., how much the affordability score changed).

We found that:

- Nationally, homes are just about the most affordable they’ve been in the last 40 years. In 2016, the median household could afford a home 1.5 times more expensive than the median home price. In 1980, the median household could only afford about 3/4 of the median home price.

- At the same time, income growth has been outpaced by home price growth. Adjusting for inflation, incomes have grown 27% between 1980 and 2016, while home prices have grown 62%.

- Despite relatively stagnant incomes, affordability has grown due to the sharp drop in mortgage rates over the last 30 years – from a high of over 16% in the 1980s to under 4% by 2016.

- Of the nation’s 100 largest metros, only Miami became unaffordable between 1990 and 2016. Meanwhile, 22 metros have flipped from being unaffordable to becoming affordable in that same time frame.

Housing Affordability Through the Ages

How much “house” you can afford depends on how your income stacks up against prevailing home prices – but mortgage rates are an X factor that homebuyers can’t control. Mortgage rates determine the size of a household’s mortgage payments– and in turn, how far their incomes can go.

It’s not your father’s housing market, at least regarding mortgage rates – and that’s a good thing. In the 1980s, the country was experiencing massive inflation. The Federal Reserve responded by driving up interest rates, which in turn led to mortgage rates in the sustained double digits, up to 16.6% in 1981. In that year, the median home price was $136,156, while the median income could only afford a home price of $97,832. In subsequent recessions–from the mild slowdowns in the early 1990s and 2000s, to the Great Recession in the mid 2000s—inflation was kept in check, and mortgage rates tended to shrink in tandem with the economy. Even in recent periods of economic expansion, such as the years following 2009, the mortgage rate continued its downward trajectory, from 5% in 2009 to less than 4% in 2016.

Turns out, changes in mortgage rates affected affordability over the years much more than changes in prices or income. If 1980’s mortgage rate came back, the median household would go from being able to afford a $312,653 home to a $144,805 home. In other words, a roughly 10% increase in mortgage rates would lead to a decrease in the affordable price by 54%.

Where Housing Became More Affordable Since 1990

Since 2012, median home prices have increased at a nominal rate of $8,644 a year, rebounding from the recession. This is notably higher than the long term rate before the recession, from 1975 to 2007 – an increase of $5,047 a year. Though it feels like the heat has been turned on in these recent years, these disparate rates of price change don’t take into account the broader picture of affordability – which, as discussed above, has changed largely due to mortgage rates. It also clouds the regional picture, which varies widely from metro to metro.

In fact, out of the top 100 metros, only one, Miami, was affordable in 1990, but became unaffordable by 2016. Twenty-two markets have experienced the opposite trend – the median household couldn’t afford the median home in 1990, but could, with money to spare, by 2016. In these metros, home prices did not outpace incomes – even if incomes fell, home prices fell even more.

Of the ten metros experiencing the highest price growth from 1990 to 2016, only three — Denver, Portland, Ore., and Miami — became more unaffordable, when stacking the median household’s affordable price against actual prices. Meanwhile, the other metros, which are relatively much more expensive, actually increased in affordability. This includes San Francisco, Seattle, and Austin, Texas. And across all ten metros, none crossed the threshold into becoming unaffordable in the last decades—if they’re unaffordable now, they’ve always been unaffordable.

Affordability, Moving Forward

Growth in home prices alone, while daunting, tends not to move the needle on median affordability that much. Recent record-low mortgage rates have created a buffer of affordability that have kept homes in most metros attainable – and at least has pulled in the reins on unaffordability in the nation’s priciest metros. Mortgage rates would have to increase by 2.5 times over the 2016 rate, to 9.4%, for the median home to become unaffordable nationally.

Of course, low mortgage rates can do little to comfort prospective buyers that find themselves priced out of certain markets. As the middle class shrinks in many parts of the country, the median household is becoming a smaller segment of the home buying market. We’ve documented the continued inventory constraint, especially on starter homes, which are attractive to household with smaller incomes. It’ll take more than just sustained low rates for buyers to feel some relief. However, recent signs of strong homebuilding may mean that relief is on the horizon.

Methodology

The Federal Housing Finance Agency’s House Price Index (HPI) was used to track house prices over time. Home price estimates in 2016 were obtained using Trulia data, and calculated over time using the HPI. For national income figures, we used Census Current Population Survey (CPS) data on median household incomes. For metro-level incomes, we used a combination of the 1990 Decennial Census and 1-Year 2016 American Community Survey data. Unless otherwise noted, home prices and incomes are inflation-adjusted using the Bureau of Labor Statistic’s CPI, all urban consumers less shelter. The maximum affordable price is calculated using median household income assuming a 20% down payment and a 30-year fixed mortgage at the annual average rate, incorporating the cost of property taxes and insurance. The affordability score was calculated by dividing the maximum affordable price by actual home prices, and multiplying by 100.