How long do you have to work in order to afford a home? Ahead of the upcoming Labor Day weekend, we calculated how many years it takes to save enough for a down payment in the 100 largest U.S. metro areas, factoring in both local average wages from the Bureau of Labor Statistics’s Quarterly Census of Employment and Wages and local housing prices based on the median asking price per square foot of homes listed on Trulia.

We assumed that people saving for a down payment set aside 10 percent of their pre-tax earnings – even though of course that depends on your earnings and how much you want to put away – and will earn an annual return of 1.5 percent on those savings. We also assumed a 20 percent down payment, the traditional norm, though many mortgages (including FHA-insured mortgages) require less than a 20 percent down payment (see note at end).

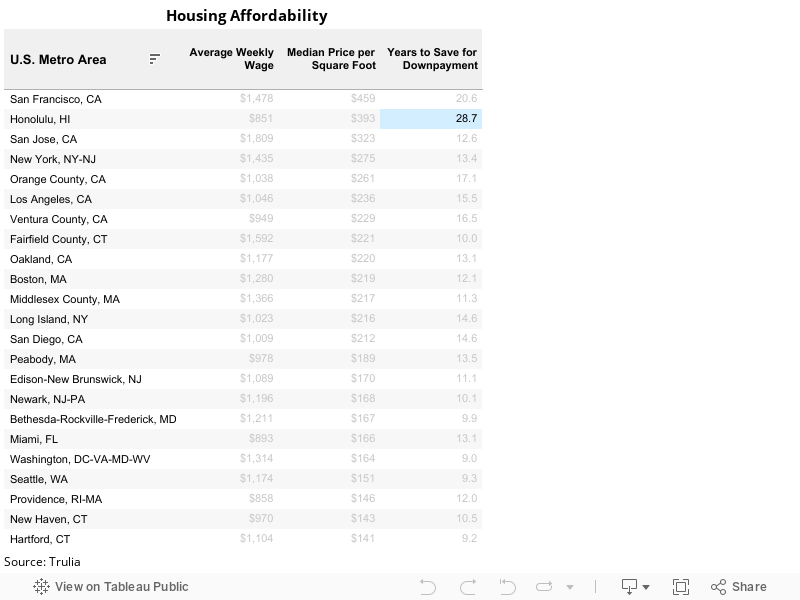

Affordability varies hugely across metro areas. Even though people can earn more money in most metros with higher housing costs – like San Francisco and New York – those high wages usually aren’t high enough to offset the even higher housing costs. We found that while wages are much higher in some metros than others, the range of home prices across metros is bigger. Among large metros, average weekly wages range from $655 in El Paso to $1809 in San Jose – almost three times as much. But median price per square foot runs from just $46 in Detroit to $459 in San Francisco – nearly ten times as high.

As the table below shows, in San Francisco you’ll need to work 20.6 years at the local average wage of $1,478 per week in order to save enough for a 20 percent down payment on a typical 2,000 square-foot home. That’s more than anywhere else in the country except Honolulu, where housing prices are high but wages are much lower.

New York is also among the 10 least affordable metros when comparing home prices to local wages. Note that six of the ten least affordable metros are located in California. With housing markets getting even tighter in California, those metros won’t get more affordable any time soon.

|

Metros with the Least Affordable Housing |

|||

| U.S. Metro |

Median price per SQFT |

Average weekly wage |

Years of savings to make a 20% down payment* |

| Honolulu, HI |

$393 |

$851 |

28.7 |

| San Francisco, CA |

$459 |

$1478 |

20.6 |

| Orange County, CA |

$261 |

$1038 |

17.1 |

| Ventura County, CA |

$229 |

$949 |

16.5 |

| Los Angeles, CA |

$236 |

$1046 |

15.5 |

| Long Island, NY |

$216 |

$1023 |

14.6 |

| San Diego, CA |

$212 |

$1009 |

14.6 |

| Peabody, MA |

$189 |

$978 |

13.5 |

| New York, NY-NJ |

$275 |

$1435 |

13.4 |

| Oakland, CA |

$220 |

$1177 |

13.1 |

At the other extreme, you’ll need to work just 3.4 years at the local average weekly wage of $1015 to buy a 2,000 square-foot home in Detroit. That’s because Detroit homes are inexpensive, not because Detroit wages are low. In fact, the average wage in Detroit is about the same as in San Diego. Texas ranks high for affordability, too: Houston and Dallas wages are above those in Los Angeles even though housing in those Texas metros is much cheaper than in southern California.

|

Metros with the Most Affordable Housing |

|||

| U.S. Metro |

Median price per SQFT |

Average weekly wage |

Years of savings to make a 20% down payment* |

| Detroit, MI |

$46 |

$1015 |

3.4 |

| Atlanta, GA |

$67 |

$978 |

5.1 |

| Houston, TX |

$84 |

$1130 |

5.5 |

| Warren–Troy– |

$77 |

$974 |

5.9 |

| Dallas, TX |

$87 |

$1057 |

6.1 |

| Indianapolis, IN |

$73 |

$871 |

6.2 |

| Memphis, TN-MS-AR |

$74 |

$878 |

6.2 |

| Las Vegas, NV |

$70 |

$818 |

6.3 |

| Fort Worth, TX |

$77 |

$896 |

6.3 |

| Cleveland, OH |

$78 |

$887 |

6.5 |

If you want more affordable housing, you might guess that moving to the suburbs is the answer. Not always! You’ll actually need to work longer – earning the local average wage – to buy a home in Long Island (14.6 years) than in New York (13.4 years); more years in Ventura County (16.5 years) than in Los Angeles (15.5 years); and more years in Peabody, Massachusetts (13.5 years), than in Boston (12.1 years).

New York, Los Angeles, and Boston all have more expensive housing than Long Island, Ventura County and Peabody, respectively, but higher wages in those urban metros relative to their suburbs more than offset higher housing prices. Homes cost 27 percent more per square foot in New York than in Long Island, for example, but average wages are 40 percent higher in New York than in Long Island.

Moving to the suburbs or a smaller city can be the key to affordability, though, if you keep your job in the big city. A down payment on a Long Island house requires only 10.7 years of earning the average wage in New York – which gets you to homeownership faster than if you paid higher New York housing prices or earned lower Long Island wages. Or, for a West Coast example, a Tacoma house takes only 6.7 years of Seattle wages. That gets you to homeownership a lot faster than living and working in Tacoma (9.3 years) or living and working in Seattle (also, coincidentally, 9.3 years).

But commuting from Long Island to New York City or from Tacoma to Seattle is no fun. If you could teleport yourself from home to work instantaneously, you might choose that commute. But why stop there? If you teleported, you could work in San Jose and live in Detroit, which would let you afford a home in just under 2 years. But be sure to program your Transporter correctly: if you accidentally ended up working in low-wage El Paso and living in high-cost San Francisco, your home would require almost 40 years of work. That’s a lot of laboring for a house.

* These estimates of years needed to save for a down payment are based on a 20 percent down payment. The years needed to save for a 10 percent down payment are slightly more than half of the years needed to save for a 20 percent down payment. It isn’t exactly half because we’re assuming that savings earn interest, which causes the total amount saved to grow exponentially, not linearly.