It turns out that you’re never too cool for school if you want to own a home.

If your dream is to own a home, getting a college degree is one of the surest ways to do so—or better yet – an advanced degree. But even without a college degree there are still places where homeownership is possible if you know where to look.

This report examines how academic degrees relate to homeownership and home size. Using the U.S. Census’ American Community Survey, we also see how the age and experience of household heads factor into housing outcomes at both the national level and among the nation’s 100 biggest metros.

Findings include:

- More education tends to lead to greater incomes and homeownership. Homeownership gains between degrees are highest when people earn high school degrees (15.9 percentage points) and bachelor’s (10.9 percentage points) degrees.

- Age and career stage also play a strong role in providing paths to homeownership. Those in the later stages of their career through retirement having the largest share of homeowners.

- Nationally, more education equates to higher levels of homeownership and larger homes. But there are still significant opportunities for those without college degrees to own homes in places such as in Long Island, N.Y. (74.5% homeownership rate for high school degree holders), Troy, Mich. (69.2%), Grand Rapids, Mich. (68.8%), and Deltona-Daytona Beach, Fla. (68.2%).

- In some metros, homeownership is a challenge no matter what degree you hold. In San Francisco and New York, for example, those with professional degrees earn median incomes of $150,000 or more, but homeownerships rates are less than 60%.

More education begets greater homeownership rates, but only to a certain point. Median incomes peak for professional degree holders (such as a medical or law degree), and with the highest academic degree—a doctorate— incomes drop back down by $17,000. As incomes rise and dip, so do homeownership rates; therefore, doctorates own homes at a rate closer to graduate degree holders, or 2.3 percentage points less than professional degree holders.

The largest jump in income, at a median increase of $35,908, is between graduate degree holders and professional degree holders. The difference between homeownership rates among these groups, however, represents the smallest rise between degrees at 2.4 percentage points. This suggests that while there may be a household income return to higher education, the homeownership returns for advanced degree holders are diminishing.

The housing outcome differences between those with and without any college degree are the starkest. Those with at least a bachelor’s degree have median incomes ($82,202) that are nearly twice those that do not ($48,842). Homeownership rates are also nearly 16 percentage points higher for those with at least a college degree, and of this more educated group that owns, homes tend to be larger with seven rooms instead of six.

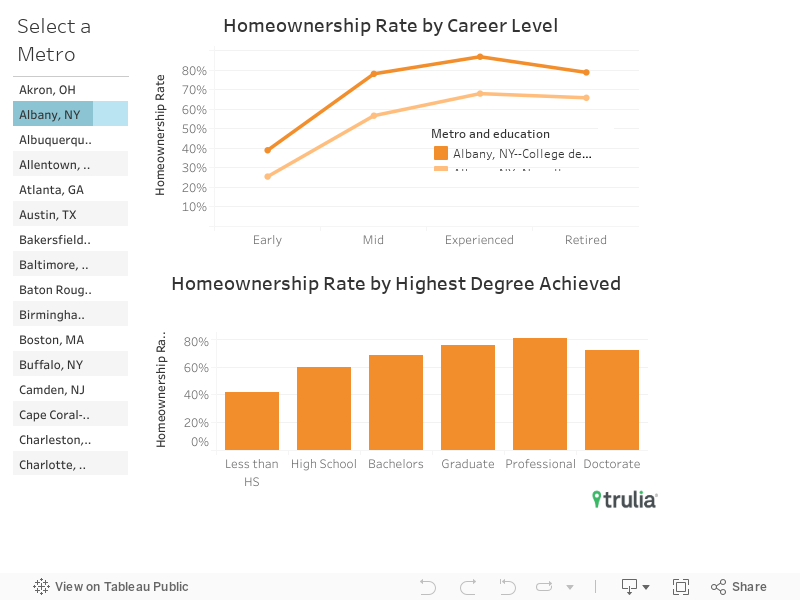

Do housing outcomes of college versus non-college degree holders differ in terms of experience and tenure? By dividing college and non-college degree holders into four career stages: 1) early career—22 to 35 year olds, 2) mid-careers—36 to 49 year olds, 3) experienced—50 to 63 year olds, and 4) retired—more than 63 years old, we see that housing outcomes across these groups consistently favor those with at least a college degree.

At every career stage, college degree holders have household incomes that are nearly twice that of non-college degree holders, with the greatest difference at the mid-career and experienced levels. Likewise, homeownership rates recorded double-digit percentage point differences across all career stages between college and non-college degree owners.

| Less than Bachelor’s Degree | Bachelor’s Degree or More | |||||

| Career Stage | Median Income | Percent Own | Median Rooms (Owners) | Median Income | Percent Own | Median Rooms (Owners) |

| Early

(Age: 22-35) |

$39,045 | 25.0% | 5 | $74,843 | 42.0% | 5 |

| Mid

(Age: 36-49) |

$51,559 | 49.2% | 5 | $106,328 | 73.4% | 7 |

| Experienced

(Age: 50-63) |

$53,000 | 63.8% | 6 | $105,387 | 82.2% | 7 |

| Retired

(Age: 63+) |

$34,040 | 68.4% | 5 | $71,182 | 81.2% | 7 |

While the national story suggests that homeownership favors the more educated, metros with the highest percentage of homeownership vary considerably across different degrees. Those who do not have a high school degree, for example still enjoy homeownership rates above 50% in metros such as Deltona-Daytona Beach, Fla. (58.9%); Gary, Ind. (55.2%); Troy, Mich. (55.1%); Grand Rapids, Mich. (55.1%); and Knoxville, Tenn. (54.5%). These markets are relatively affordable, with median home values below the national median of $200,400.

Long Island, N.Y. tops metros for homeownership (74.5%) among those with high school degrees and also has the highest homeownership rate (79.6%) overall among the biggest 100 metros.

High Homeownership Rates for Those With Less Than a High School Degree

While more education is linked to higher homeownership, there is a cost to obtaining academic degrees. According to the Federal Reserve Bank of New York’s recent household debt survey, student loan debt has more than doubled in the past 10 years. Many graduates in the past decade feel the burden of paying back student loans as they try to save for their first home. However, early career college degree holders consistently have higher homeownership rates than those without a degree, suggesting that despite this debt, more education still pays.

For those with higher education degrees some places offer especially strong opportunities for homeownership. Professional degree holders in Louisville, Ky., for example, have homeownership rates of 86.1% compared to 67.2% homeownership overall. The concentration of universities in the Jacksonville, Fla., translates to 86.4% of doctorates owning homes, more than 20 percentage points more than the metro-wide rate.

In some metros, homeownership is a challenge no matter what degree you hold or how much your household makes. San Francisco, for example, sits in the bottom five of the biggest 100 metros in terms of homeownership across all degree holders. With the median home valued at nearly $1.2 million, even professional degree holders with median household earnings of $174,000 see a homeownership rate of 58.2%.

Those early in their careers, or those between 22 and 35, struggle mightily to own a home in San Francisco. The difference between homeownership rates between those with a college degree or higher and those without one is just 9 percentage points, or 19% and 11% respectively. Most surprising about this figure is that in San Francisco those who hold a college degree or more and are early in their careers make more than double those young people without college degrees ($117,735 versus $50,058).

Other metros where homeownership rates are low across the board include New York, Boston, Los Angeles, and Honolulu. These areas are some of the most expensive housing markets in the country and have some of the smallest margins between the cost of renting versus buying.

Methodology

Data for this report are from the U.S. Census’ 2015 5-Year American Community Survey (ACS). The Census microdata are accessed from IPUMS-USA, University of Minnesota. Education levels are based on all household heads over the age of 22, but income represents household income. This report focuses on the biggest 100 metros according to the number of occupied housing units, and national data figures from the 100 metros weighted by their number of occupied housing units.

According to the Census ‘high school’ includes both high school degrees as well as GEDs or alternative credentials equivalent to a high school degree. ‘Grad’ degrees are master’s degrees such as an MA, MS, MEng, MSW or MBA. ‘Professional’ degrees include MD, DDS, DVM, LLB and JD.

Career stages are defined by Trulia in terms of age as follows: early career (those aged 22 to 35), mid-career (aged 36 to 49), experienced (aged 50 to 63) and retired (over the age of 63).

Steven Ruggles, Katie Genadek, Ronald Goeken, Josiah Grover, and Matthew Sobek. Integrated Public Use Microdata Series: Version 6.0 2015. Minneapolis: University of Minnesota, 2015. http://doi.org/10.18128/D010.V6.0